The Federal Housing Administration (FHA) Mortgagee Letter (ML) 22-17 announced that FHA’s Technology Open To Approved Lenders (TOTAL) Mortgage Scorecard will begin scoring a borrower’s positive rental payment history as part of the credit risk analysis when they are applying for FHA-insured financing.

TOTAL will begin scoring on or after October 30, 2022, as well as for case numbers assigned on or after September 20, 2021, allowing lenders to implement the guidance on existing pipeline cases without the need to obtain a new case number.

We have the expertise to manually underwrite even the most difficult Kentucky FHA Mortgage loans. Whether it’s purchase or refi—we work hard to approve what other lenders won’t.

Did you know over 50% of our Kentucky FHA loans are manual underwrites?

Kentucky FHA will consider the borrower’s entire story, including extenuating circumstances and compensating factors, to justify loan approvals. If your borrower falls under any of these conditions, they may benefit from manual underwriting:

Non-traditional credit / lack of credit

True extenuating circumstances affecting credit or income history

Lack of seasoning on a Chapter 13

Disputed accounts over $1,000

Frequent job changes in the last 12 months

If you think your borrower could benefit from manual underwriting call us to learn more about manual underwriting or submit your scenario today.

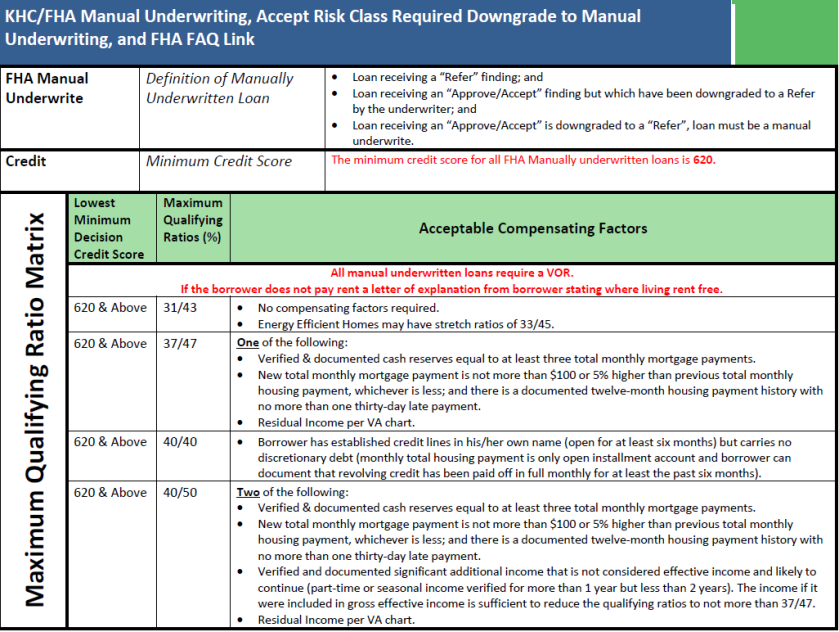

Lowest Minimum Decision Credit Score Maximum Qualifying Ratios (%) Acceptable Compensating Factors All manual underwritten loans require a VOR. If the borrower does not pay rent a letter of explanation from borrower stating where living rent free. 620 & Above 31/43 • No compensating factors required. • Energy Efficient Homes may have stretch ratios of 33/45. 620 & Above 37/47 One of the following: • Verified & documented cash reserves equal to at least three total monthly mortgage payments. • New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less; and there is a documented twelve-month housing payment history with no more than one thirty-day late payment. • Residual Income per VA chart. 620 & Above 40/40 • Borrower has established credit lines in his/her own name (open for at least six months) but carries no discretionary debt (monthly total housing payment is only open installment account and borrower can document that revolving credit has been paid off in full monthly for at least the past six months). 620 & Above 40/50 Two of the following: • Verified & documented cash reserves equal to at least three total monthly mortgage payments. • New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less; and there is a documented twelve-month housing payment history with no more than one thirty-day late payment. • Verified and documented significant additional income that is not considered effective income and likely to continue (part-time or seasonal income verified for more than 1 year but less than 2 years). The income if it were included in gross effective income is sufficient to reduce the qualifying ratios to not more than 37/47. • Residual Income per VA chart.

KENTUCKY FHA MORTGAGE MANUAL UNDERWRITING GUIDELINES FOR VA RESIDUAL INCOME

Residual Income Calculating Residual Income Residual income is calculated in accordance with the following: • Calculate the total gross monthly income of all occupying borrowers • Deduct from the gross monthly income the following items: ➢ State income taxes ➢ Federal income taxes ➢ Municipal or other income taxes ➢ Retirement or Social Security ➢ Proposed total monthly fixed mortgage payment ➢ All recurring monthly debt obligations ➢ Estimated maintenance and utilities ($0.14 x sq. ft.) ➢ Job related expenses (e.g., child care) • The difference between the gross monthly income and the deductions above is the residual income Compensating Factors Using Residual Income as a Compensating Factor Count all members of the household of the occupying borrowers without regard to the nature of their relationship and without regard to whether they are joining on title or the note. Exception: As stated in the VA Guidelines, the mortgagee may omit any individuals from “family size” who are fully supported from a source of verified income which is not included in the effective income in the loan analysis. These Individuals must voluntarily provide sufficient documentation to verify their income to qualify for this exemption. From the table below, select the applicable loan amount and household size. If residual income equals or exceeds the corresponding amount on the table, it may be cited as a compensating factor.

Kentucky FHA Mortgage Manual Undewriting Guidelines for FHA Mortgage Refer Eligible or Manual Downgrades Compensating Factors for Manual FHA approval

Accept Risk Class required downgrade to Manual Underwriting The Mortgagee must downgrade and manually underwrite any mortgage that received an accept or approve/eligible recommendation if: • The mortgage file contains information or documentation that cannot be evaluated by TOTAL. • Additional information, not considered in the AUS recommendation affects the overall insurability of the mortgage. • The borrower has $1,000 or more collectively in Disputed Derogatory Credit Accounts. • The date of the borrower’s bankruptcy discharge as reflected on bankruptcy documents is within two years from the date of the case number assignment. • The case number assignment date is within three years of the date of the transfer of title through a Pre-Foreclosure Sale (Short Sale). • The case number assignment date is within three years of the date of the transfer of title through a foreclosure sale. • The case number assignment date is within three years of the date of the transfer of title through a Deed-in-Lieu (DIL) of foreclosure. • The Mortgage Payment history, for any mortgage trade line reported on the credit report used to score the application, requires a downgrade as defined in Housing Obligations/Mortgage Payment History. • The Borrower has undisclosed mortgage debt that requires a downgrade. • Business income shows a greater than 20 percent decline over the analysis period.

FHA loans with case numbers assigned on and after June 1, 2022.

Appraisal Validity Period

Loans with case numbers assigned prior to June 1, 2022

Loans with case numbers assigned on and after June 1, 2022

• The initial appraisal validity period is 120 days from the effective date of the appraisal.

• The 120-day validity period may be extended for 30 days at the option of the underwriter if the conditional commitment is issued before the original appraisal expiration date.

The following update aligns with FHA Mortgagee Letter 2022-11 and is effective for all FHA loans with case numbers assigned on and after June 1, 2022. Appraisal Validity Period Loans with case numbers assigned prior to June 1, 2022 Loans with case numbers assigned on and after June 1, 2022 • The initial appraisal validity period is 120 days from the effective date of the appraisal. • The 120-day validity period may be extended for 30 days at the option of the underwriter if the conditional commitment is issued before the original appraisal expiration date. • An appraisal update may be used to extend the validity period of the initial appraisal. The appraisal update must be performed before the initial appraisal with no extension has expired. • When the initial appraisal is updated, the updated appraisal will be valid for 240 days after the initial appraisal effective date. • The initial appraisal validity period is 180 days from the effective date of the appraisal. • If the initial appraisal will be more than 180 days at the disbursement date, an appraisal update may be performed to extend the appraisal validity period. • When the initial appraisal is updated, the updated appraisal will be valid for one year after the initial appraisal effective date. With these updates, the optional 30-day extension is no longer necessary and has been eliminated. In addition, the requirement for the appraisal update to be performed before the initial appraisal has expired has been removed.

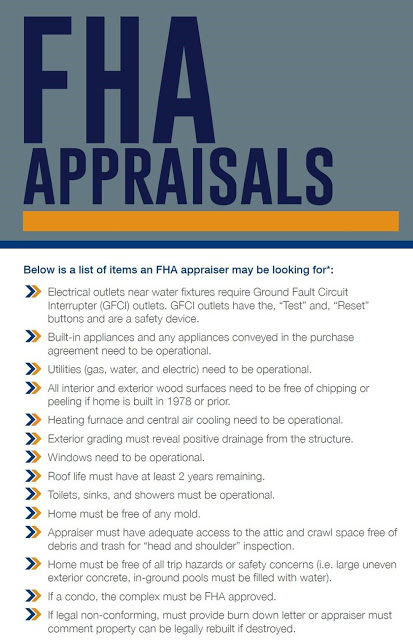

Kentucky FHA Appraisal Requirements For A Mortgage Loan Approval.

Applies to case numbers assigned on or after June 1, 2022

Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report;

Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report;

Allows the appraisal update to be ordered AFTER an appraisal expires; and

Eliminates the optional 30-day extension.

✨This is big news for FHA ✨

The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.

Kentucky FHA Appraisal Requirements For A Mortgage Loan Approval.

Ordered through a third party source. Interested/vested parties may not initiate the appraisal. I.E> buyers, sellers, realtors, loan officer, family members

Property must meet HUD’s minimum property standards. i.e.: permanent heat source, utilities must be on and in working order at time of inspection

Flips < 90 days – not allowed Per HUD -If current owner owned less than 90 days FHA will not insure. Sometimes a second appraisal will be required by FHA investor if sold within the last 6 months for a large profit. Receipts of work done may be needed to substantiate increase in value of home in short-time period.

Transferred appraisal – ok

Appraisal valid 120 days – 30 day extension possible*

Property eligibility – No location restrictions.

New Construction Available

Kentucky FHA Appraisal Requirements For A Mortgage Loan Approval.

FHA MORTGAGE LOANS AND FLIPPING RULE FOR APPRAISALS

Resales Occurring 90 Days or Fewer after Acquisition:

Not eligible for FHA financing

Resales occurring between 91 days and 180 Days after Acquisition:

Obtain 2nd appraisal if resold between 91 to 180 days after acquisition

Obtain 2nd appraisal if resale price is 100% or more over price paid by seller

If 2nd appraisal is more than 5% lower than value of first appraisal, the lower value must be used

Borrower not allowed to pay for 2nd appraisal

Exceptions to FHA Flipping Rules:

Property purchased by an employer or relocation company due to relocation of an employee

Resales by HUD – REO program

Sales by other government agencies (i.e., IRS, court-ordered, DEA, etc.)

Sales of non-profit agencies approved to purchase HUD properties

Acquisition due to inheritance

Sales of properties by federally chartered financial institutions

Sales of properties by GSE’s

Sales of properties by local or state governments

Sales by builders selling a new home

Sales of properties in federally declared disaster areas

NOTE: Mortgage Company must obtain a 12-month chain of title to document time restrictions above. VA MORTGAGE AND FLIPPING RULE

No Flipping Rules – Overlays may apply or at Underwriter’s discretion

USDA RURAL HOUSING MORTGAGE FLIPPING RULES

Lender is responsible to ensure that any recently sold property’s value is strongly supported when a significant

increase between sale and purchase occurs.

Lender must ensure that the appraisal value is supported with validated comps and protect the borrower from

predatory lending.

Fannie Mae Appraisal Flipping Rules

No Flipping Rules – Lender overlays may apply

Freddie Mac

No Flipping Rules – Lender overlays may apply

Applies to case numbers assigned on or after June 1, 2022

Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report;

Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report;

Allows the appraisal update to be ordered AFTER an appraisal expires; and

Eliminates the optional 30-day extension.

✨This is big news for FHA ✨

The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.

Kentucky FHA appraisals can take home buyers by surprise. That’s why we’ve put together some good-to-know info about the process. Feel free to use this to help educate your clients.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.