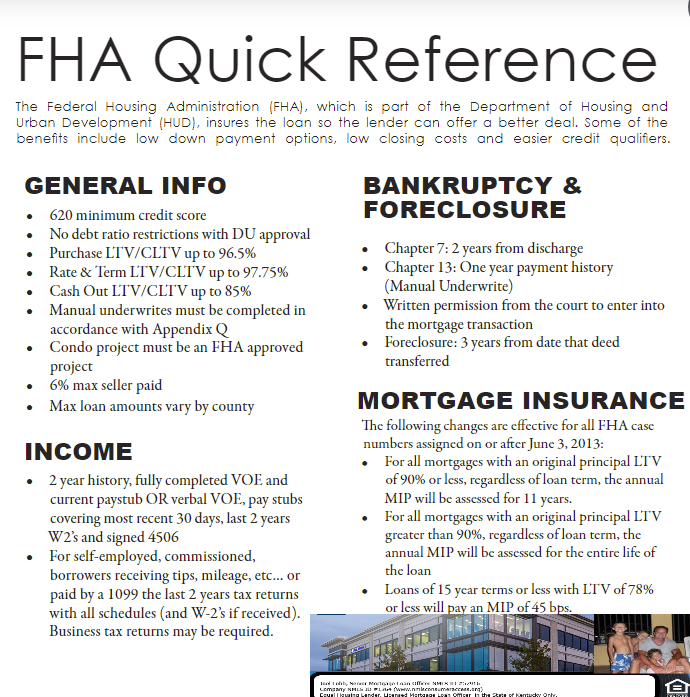

How to Calculate Income for a Kentucky FHA Mortgage Approval?

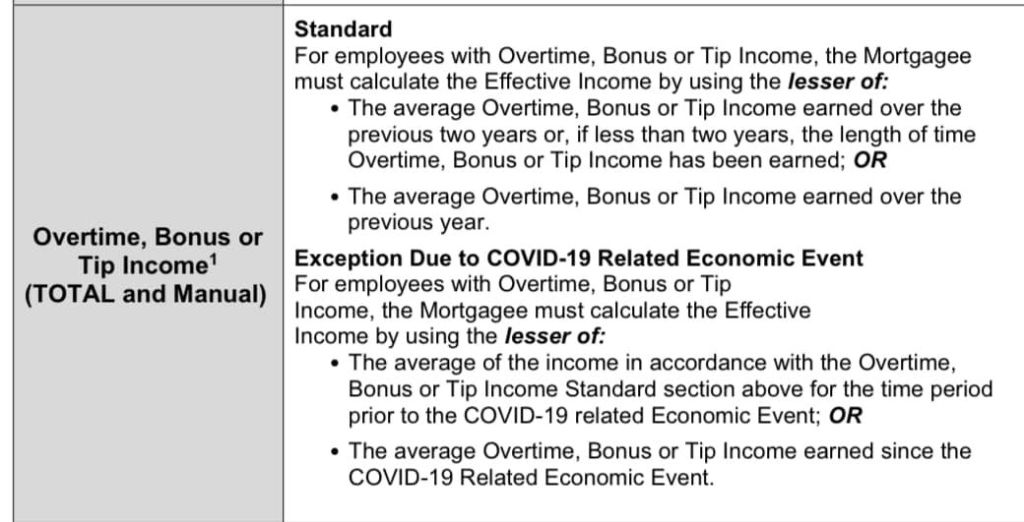

FHA INCOME CALCULATION FOR OVERTIME, BONUS, TIP INCOME FOR KENTUCKY FHA LOANS

FHA INCOME CALCULATION FOR OVERTIME, BONUS, TIP INCOME FOR KENTUCKY FHA LOANS

FHA has published the following guideline updates, which will be effective for all Kentucky FHA loans

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

Text or call phone: (502) 905-3708

email me at kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

This web site is not the FHA, VA, USDA, HUD or any other government organization responsible for managing, insuring, regulating or issuing residential mortgage loans.

**Download Fair Housing Booklet – CLICK HERE

All approvals and rates are not guaranteed, and are only issued based on standard mortgage qualifying guidelines

Remember, we are even available this weekend for pre-qualifications or questions. Call our cell phone or email us. If you miss us, leave a message and we WILL call you back

Your debt-to-income ratio, technically speaking, is all of your monthly debt payments divided by your gross monthly income—that is, the percentage of your gross monthly income that goes towards payments for rent, mortgage, credit cards, and other debt. This is how lenders measure your ability to manage the monthly mortgage payments to repay the money you’ll be borrowing.

To calculate your debt-to-income ratio, add up your monthly debts—this includes car payments, credit cards, mortgages, and student loans. Divide this amount by your monthly gross income, and you’ll get your DTI ratio.

For reference, the standard maximum DTI for conventional loans is 45%, and for FHA loans it’s 55%. Of course, the maximum DTI depends on the home loan.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle Louisville, KY 40223

Company NMLS ID #1364

click here for directions to our office

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

https://www.mylouisvillekentuckymortgage.com/

Kentucky FHA Temporary Guideline Changes:

Rental Income & Self-Employment Income

FHA Announces COVID-19 Temporary Guidance for Kentucky FHA Mortgage Loans

Due to the ongoing effect of COVID-19, FHA has announced in ML 2020-03, updates to the following temporary guidelines below effective with case number assignments on or after 8/12/2020 -11/30/2020:

Rental Income for Kentucky FHA Mortgage Loans

Self Employment Income for Kentucky FHA Mortgage loans

Text/call: 502-905-3708