Chapter 2

Mortgage Credit Guidelines

Page 2-19

A refinance transaction involves paying off an existing real estate debt from proceeds of a new mortgage. For all refinance loan transactions, 1) the borrower must be current for the month due and, 2) there must a current payoff statement in the case binder.

Under the terms and conditions outlined below, FHA will insure the following types of refinances:

A. Regular Refinances – “cash-out” and “no cash-out”

1. “Cash-Out” Refinances: the maximum loan-to-value and combined loan-to-value of any cash-out refinance is 85%. The calculation is based either off the appraised value or the original sales price, depending on the length of time the borrower has owned the property.

a)The loan is limited to a combined LTV (FHA insured first mortgage and any subordinated lien) of 85% of the appraised value, provided the borrower has owned the property for at least one year. Note that manufactured homes have other restrictions (Handbook 4155.1, section 3.A).

b) If the property was purchased less than one year preceding the application date, the LTV/CLTV (85%) for the mortgage amount must be calculated using the lesser of the appraised value or the original sales price of the property.

c) The property that is security for the refinanced mortgage may be a 1-4 unit property.

d)The property must be owner-occupied. Non-owner occupant co-borrower may not be added in order to meet FHA?s credit underwriting guidelines.

e)Properties owned free and clear may be refinance as cash-out transactions.

f)3-4 unit properties are required to pass the self sufficiency test and have a minimum of 3 months reserves after closing.

g) Properties acquired by inheritances within the past 12 months are eligible for a cash-out refinance transaction provided they have been occupying the property as their primary residence since the inheritance. The lender must document the acquisition by the borrowers via inheritance.

h)Manufactured homes: there are restrictions applicable please refer to Handbook 4155.1, section 3.A.

2.No Cash-Out Refinances (non-streamline): The maximum mortgage is based on the lesser of “a” and “b” below (a third calculation is applicable if owned less than 12 months):

a)The maximum LTV percentage is multiplied by the appraised value, exclusive of closing costs (please refer to Mortgagee Letter 2010-24).

b)The sum of the existing first lien, any purchase money second mortgage and/or any junior liens over 12 months old, closing costs, prepaid expenses, accrued late charges, escrow shortages, borrower paid repairs required by the appraisal, discount points, prepaid penalties charged on a conventional loan and FHA Title 1 loans as determined by the appropriate HOC subtract any refund of refund of upfront MIP. Note that the prepaid expenses may include per diem interest through the end of the month for the new loan, hazard/flood insurance premiums, mortgage insurance premiums and property tax deposits needed to establish the escrow account. The existing first lien may include the interest charged by the servicing lender, when the payoff is not received by the first of the month, but may not include any delinquent interest.

c)If the property was acquired less than one year before the loan application, and the existing loan is not an FHA loan, the original sales price, must be considered in calculating the maximum mortgage. Refer to Handbook 4155.1, section 3.B.

d)There may not be more than $500 in incidental cash back to the borrower.

e)If there is an existing subordinate lien refer to Handbook 4155.1, section 3.A, 3.B and ML 11-11.

f)Additional restrictions apply for manufactured homes; refer to Handbook 4155.1, section 3.A.

B.Streamline Refinances (with or without an appraisal): Streamline transactions involve the refinance of the FHA insured first mortgage only. This type of loan is designed to lower the monthly principal and interest payments on the current FHA insured mortgage and involves no cash back to the borrower. All Streamline transactions must meet the following criteria:

Note: Effective with case numbers assigned on or after April 18, 2011, the use of an appraisal to increase the insurable mortgage balance for a “non-qualifying” streamline refinance will no longer be permitted.

I)At the time of loan application: a) the borrower must be current, b) must have made at least 6 full months of payments since the first payment date and, c) at least 210 days must have passed from the closing date of the mortgage being refinanced.

2)At the time of loan application the borrower must exhibit an acceptable payment history as described below:

a) For mortgages with less than a 12 month payment history, the borrower must have made all mortgage payments within the month due.

b)For mortgages with a 12 month payment history or greater, the borrower must have:

i)Experienced no more than one 30 day late payment in the preceding 12 months, AND

ii)Made all mortgage payments within the month due for the three months prior to the date of loan application.

III)The lender must determine there is a net tangible benefit as a result of the streamline refinance transaction, with or without an appraisal. Net Tangible benefit is defines as:

a) Reduction to the principal, interest plus MIP by at least 5% (compare the new P & I & MIP to the existing P & I & MIP), or

b) For details of permissible minimum thresholds involving refinancing in or out of an ARM refer to ML 2011-11.

4)Investment/secondary property: for FHA financed properties that have become investment properties or secondary residences, a streamline refinance is only permitted without an appraisal. All other criteria must be met, however these properties may not be refinanced into an ARM.

5) Assets: If assets are needed to close, they must be verified.

6)A current payoff statement must be in the case binder.

7) Subordinate financing: if subordinate financing will remain in place, the maximum CLTV is 125%. To calculate the maximum CLTV for streamlines without an appraisal, use the “original property value” shown on the Refinance Authorization screen in FHAC. For streamlines with an appraisal, the CLTV calculation is based on the new appraised value.

8)LDP and GSA lists are required to be checked, however there is no need to check the CAIVRS.

9)URLA: for non-credit qualifying streamlines an abbreviated version of the URLA is permitted, however for credit qualifying streamlines, a fully completed URLA is required.

10)Maximum mortgage:

a) Streamline refinance without an appraisal (owner occupied): the maximum mortgage is the outstanding principal balance plus interest charged by the servicing lender (but may not include delinquent interest, late charges or escrow shortages), minus UFMIP refund plus new UFMIP.

b) Streamline refinance with an appraisal: as reflected above for case number assigned on or after April 18, 2011. For cases with case numbers assigned prior to this date refer to Handbook 4155.1, section 6.C.

c) Streamline refinance without an appraisal (non-owner occupied): these may only be refinanced without an appraisal and the new base mortgage may only cover the outstanding principal balance less the any UFMIP refund. Further the term of the mortgage must be the lesser of 30 years or the remaining term of the mortgage plus 12 years.

Website Fine Print

The content provided on this website is presented or compiled by Joel Lobb and is provided for informational purposes only. It does not necessarily represent the views or opinions of Key Financial Mortgage .Neither Joel Lobb nor Key Financial Mortgage assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information disclosed, or represents that its use would not infringe privately owned rights.

The mortgage or financial services or strategies mentioned in this website may not be not suitable for you.

Key Financial Mortgage is an Equal Opportunity Lender. All rights Reserved.

Joel Lobb is a Licensed Mortgage Originator:NMLS #57916. Key Financial Mortgage NMLS # 1800 is a licensed Mortgage Broker Company in the State of Kentucky

Legal Disclaimer

*

*

This web site is not the FHA, VA, USDA, HUD or any other government organization responsible for managing, insuring, regulating or issuing residential mortgage loans.

**Download Fair Housing Booklet – CLICK HERE

All approvals and rates are not guaranteed, and are only issued based on standard mortgage qualifying guidelines.

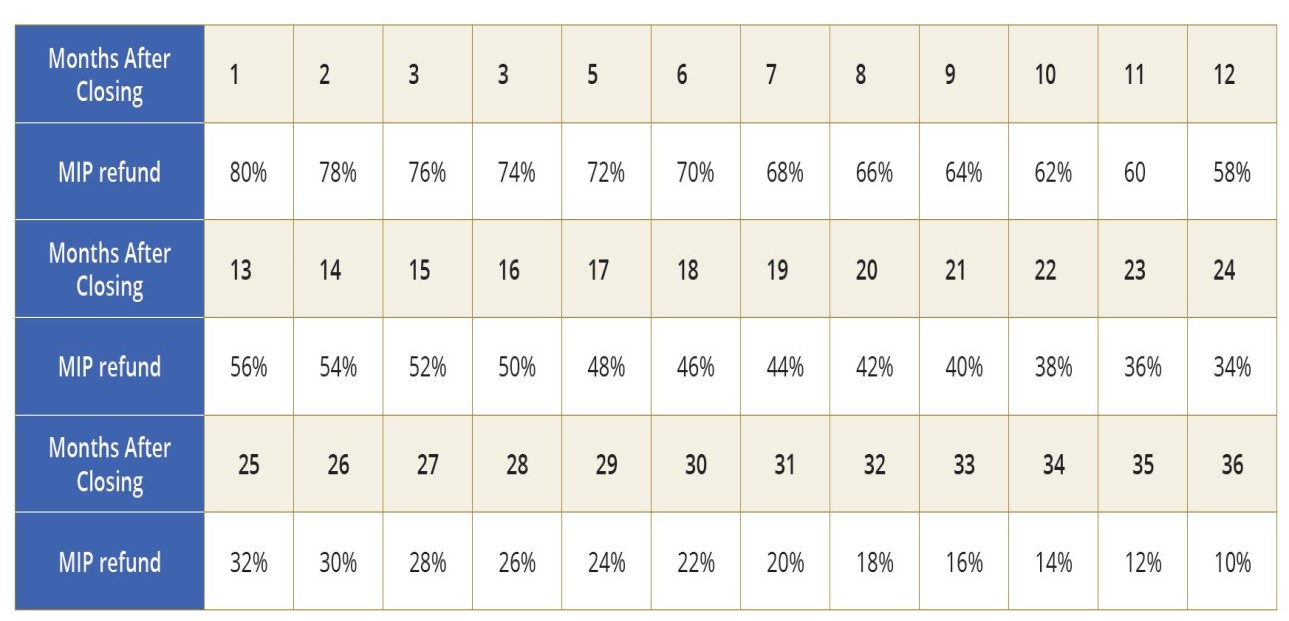

How do you get back a

How do you get back a