Category: kentucky mortgage requirements

Qualifying for an FHA Loan in Kentucky

When it comes to buying a home in Kentucky, FHA loans are a popular choice for many first-time homebuyers due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know: Understanding these … Continue reading “Qualifying for an FHA Loan in Kentucky”

When it comes to buying a home in Kentucky, FHA loans are a popular choice for many first-time homebuyers due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

- Credit Score Requirements:

- FHA loans are known for accommodating borrowers with lower credit scores. While the minimum required credit score can vary, typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. However, borrowers with credit scores between 500 and 579 may still be eligible with a higher down payment, usually around 10%.

- Down Payment:

- The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

- Work History:

- Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history, preferably with the same employer or within the same field, helps demonstrate financial stability and the ability to repay the loan.

- Debt-to-Income Ratio (DTI):

- The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income and can go higher up to 56% with good credit scores, large down payment or shorter term loan although lenders may consider higher ratios in certain cases if compensating factors are present.

- Bankruptcy and Foreclosure:

- FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

- Mortgage Term:

- FHA loans offer various mortgage term options, including 15-year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

- Occupancy: Primary residences not for rental properties

- Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

- can be used for refinances, not only for purchases.

- Max FHA loan in Kentucky is $498,257. This changes every year

- No income limits nor property restrictions on where home is located

- Can close within 30 days typically with good appraisal and title work

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can also provide valuable guidance and assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

Kentucky FHA Loan Requirements For 2024

How to Qualify for a Kentucky FHA Mortgage Loan with a lender in Kentucky?

The requirements for Kentucky FHA loans are set by HUD.

- Borrowers must have a steady employment history of the last two years within the same industry or line of work. Recent college graduates can use their transcripts to supplant the 2-year work history rule as long as it makes sense.

- Self-Employed will need a 2-year history of tax returns filed with IRS. They will take a 2-year average.

- FHA requires a 3.5% down payment. Can be gifted from a family member or from a retirement savings plan, or money saved up. Any type of cash deposits is not allowed for down payments. No exceptions to this rule!! This is one of the biggest issues I see in FHA underwriting nowadays.

- FHA loans are for primary residence occupancy. Not rental houses.

- Borrowers must have a property appraisal from an FHA-approved appraiser.

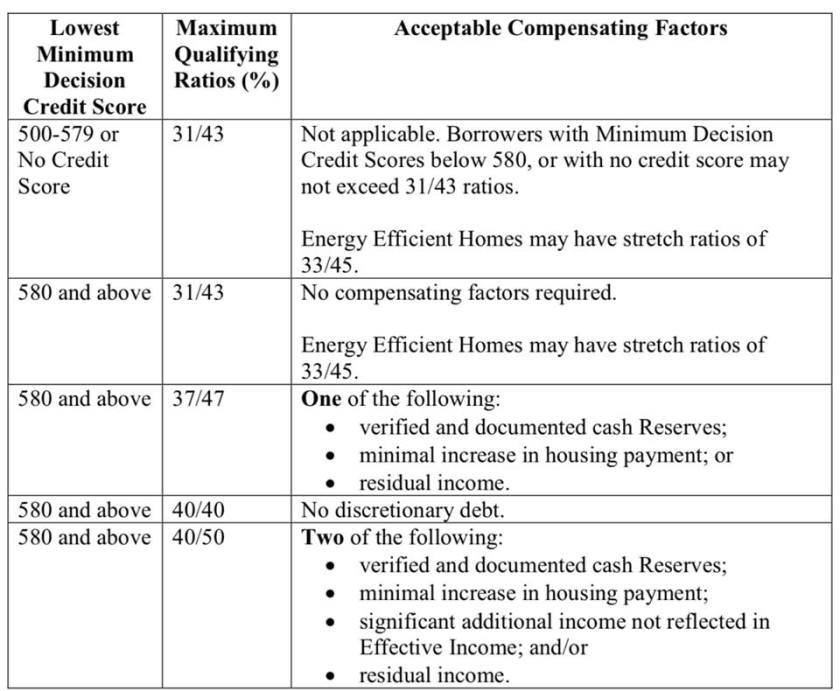

- Borrowers’ front-end ratio (mortgage payment plus HOA fees, property taxes, mortgage insurance, homeowners insurance) needs to be less than 31 percent of their gross income, typically. You may be able to get approved with as high a percentage as 43 percent. If the Automated Underwriting System gives you an Approved Eligible you can go higher on the debt ratios

- Borrowers must have a minimum credit score of 580 for maximum financing with a 3.5% down payment

- Borrowers must have a minimum credit score of 500-579 for maximum LTV of 90 percent with a minimum down payment of 10 percent. Most lenders will not go below 580 to 620 score, and very few lenders will go to 580 score. It’s best to work on getting your scores up before you apply or work with a loan officer to improve them.

- 2 years removed from Chapter 7 is required with good pay history after bankruptcy

- 1 year removed from Chapter 13 is okay with an excellent pay history with the Chapter 13 plan and permission from the trustee. You will need to qualify with the Chapter 13 payment along with a new house payment. Again, scores will play into your loan pre-approval.

- Typically borrowers must be three years out of foreclosure and have re-established good credit. Exceptions can be made if there were extenuating circumstances and you’ve improved your credit. If you were unable to sell your home because you had to move to a new area, this does not qualify as an exception to the three-year foreclosure guideline.

- The property must be appraised by a Kentucky FHA-approved appraiser.

- The property must be safe, sound and secure, in compliance with minimum property standards as defined by the U.S. Department of Housing and Urban Development, or HUD.

- You may not have delinquent federal debt or judgments, or debt associated with past FHA loans. Caivrs Alert System will show up if you owe the government money.

Why Lenders Use CAIVRS

It is true that your CAIVRS report can help lenders to predict the risk of doing business with you, just like a traditional consumer credit report. But the primary reason lenders check your CAIVRS report is because they are generally required to do so for any applications that involve a federal loan (FHA, VA, USDA, SBA, etc.). Lenders are required to conduct a CAIVRS search because of Title 31 of the United States Code (Section 3720B) bars “delinquent federal debtors from obtaining federal loans or loan insurance guarantees.”

Kentucky FHA Loan Requirements for 2024

-

Gift Rules for Down-Payment Sources Guidelines on FHA Mortgage Programs

One of the biggest obstacles to buying a home for Americans is the down payment. There was a time when you needed a 20% down payment and a high credit score to buy a home. But in 2022, you can buy a home with average to below-average credit and low down payment in some cases. One of the most popular loan programs for these buyers if the FHA loan. A major advantage of the FHA mortgage loan is you can get approved with only a 3.5% down payment with a 580 or higher credit score. If you have a lower score than that, you need a 10% down payment.

Still, there are situations where the borrower is having trouble coming up with the down payment for the loan. What to do then? FHA guidelines do allow other options. Keep reading to learn more.

More on FHA Down Payments and Approved Sources

As we noted above, you are required to have at least a 3.5% down payment to be approved for an FHA loan. The money must be verified by the FHA-approved lender to come from an ‘approved source.’ What is an approved source, anyway? Most people get their down payment from cash reserves, investments, borrow from 401k or IRA, etc. The idea behind verifying where the money came from is to make sure the borrower did not get the down payment from a credit card or payday loan, etc.

But there are other options for your down payment. The funds also can come from a gift. The gift and the giver do need to meet FHA requirements, but this flexible guideline makes it possible to get into an FHA loan with, technically, zero money down. To determine if the down payment gift can be used or not, it is necessary to check HUD rules. According to HUD 41.55.1 Chapter 5 Section B, for the funds to be a gift, there cannot be any expected repayment of the money.

Also, FHA will scrutinize the giver of the gift. Chapter 5 of the HUD Code states the cash gift is OK if it comes from your relative; employer or labor union; close friend with a defined interest in you; charitable organization; government agency or public entity.

FHA also states who cannot give gift funds to you for the down payment. These are the seller; the real estate agent or broker on the deal; the builder or an associated entity.

Gift Terms Explained

The gift for your down payment cannot be made based upon paying it back later. You are required to get a gift letter from the person or organization. The letter should state that you are not required to pay the money back. It also should provide the contact information for the borrower, such as name, address, and phone number. Also included should be the bank account from which the funds will be sent.

The gift donor should be OK with giving a bank statement with the letter. Also, he or she should ensure that the transfer amount matches what is in the gift letter and what is deposited into your account.

FHA rules are very specific on these areas to ensure that the home buying process through FHA is fair and just. But as long as you follow the FHA rules, you should be able to get help with your down payment from a friend or relative.

Don’t Have Friends or Family Who Can Help?

Not every borrower has friends or family who can give them a gift for their down payment. But HUD lists many government programs spread throughout the country in most states that can offer down payment and closing cost help for certain borrowers.

It also is worth checking if your employer and state have employer-assisted housing. This program can help people with moderate incomes to get a loan to cover closing costs and down payment. Look up FHA in your state on Google to see what is available.

The FHA is actually not the lender. They insure the loans that are issued by FHA-approved lenders. FHA loans are gear more toward borrower’s with less than 20% down payment and credit issues in the past.

Qualifying for a FHA Loan Mortgage In Kentucky

Credit Scores and Down Payment Percentages – Each year, the rules for qualifying for these loans changes. For 2024, applicants need a minimum credit score of 580 in order to get the low down payment, which is 3.5 percent.

For those whose credit score is less than 580, they will have to come up with 10 percent for their down payment. This does not guaranteed a mortgage loan approval if you have the certain credit scores, just a the minimum required.

Compensating Factors for FHA loan Approval

The credit score is just one part of the story. The FHA will also evaluate the borrower’s bankruptcies, foreclosures, prior payment history on other debts. They will also want information on difficulties that kept the borrower from making payments on other debts in the past.

Negative strikes against qualifying for the loan include not having any credit history or a bankruptcy.

Someone with a bankruptcy will have to wait for two or more years after their bankruptcy before applying for an FHA-insured loan.

If you have late payments on debt obligations, it is best to wait until you have had a full year of on-time payments before you apply for a FHA-insured loan.

If you have had a foreclosure in the past, you may still be able to get a FHA-insured loan three years after your foreclosure. The lender will be looking at the circumstances behind the foreclosure.

If you have had any civil judgement against you for money owed, collections actions or unpaid/unresolved federal debt, the FHA-approved lender will be required by the FHA to establish that all of these outstanding issues are resolved or paid before you can go through closing.

Watch out for student loans if they are delinquent because sometime this can cause a lien against you in the form of a CAVIRS Alert with HUD

As you can see, many types of borrowers who would not be eligible for a traditional mortgage, or who would face exorbitant interest rates, will be able to qualify for a FHA-insured loan at attractive interest rates.

Employment and Income for a Kentucky FHA Loan

You must have an employment history that is steady for the last two years. Does not have to be same employer.

Your income has to be verifiable in some way, whether that be through pay stubs, your income tax returns. No bank statements or cash deposits , or undocumented income can be used for income qualifying purposes.

Debt-to-Income Ratio Requirements –

Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.

Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.

If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Property Requirements for a Kentucky FHA Loan

It must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.

It is really not too hard to pass FHA loans and the appraisal process.

Pros of FHA Loans –

-

New homebuyers and those who have lower credit scores or who have other blemishes on their credit history will often qualify for FHA-insured loans.

-

Even though these borrowers are considered “subprime” to a traditional lender, they will receive attractive interest rates through the FHA-insured mortgage programs.

-

The down payments required from borrowers are lower than those required by traditional mortgage lenders.

-

These loans can be combined with other forms of public assistance for lower income or new borrowers so that the borrower will not need to come up with a down payment of any kind.

Cons of FHA Loans –

-

Since the FHA is not actually the lender, and you have to go through FHA-approved lenders, you may not qualify due to stricter standards that the lender has for the loan.

-

Because you are not paying 20 percent as a down payment, the FHA requires two mortgage insurance premiums to be paid. One is an upfront premium that is 1.75 percent of the loan amount. Lenders often will allow you to make that mortgage insurance premium a part of your loan. The second is an annual mortgage insurance premium that is .45 percent or 1.05 percent. This premium is paid monthly.

FHA FINANCING

CREDIT REQUIREMENTS FOR KENTUCKY FHA FINANCING

What credit score do I need to qualify for a Kentucky FHA loan is one of the most common questions I hear from Kentucky homebuyers?

The short answer is you must have a minimum credit score of 500 to be eligible for an FHA loan in Kentucky. Anything lower than 500 disqualifies you from consideration for an FHA loan.

There are two sets of credit score requirements for a Kentucky FHA Loan

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default.

You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an Kentucky FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them.

This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

-

-

Joel Lobb (NMLS#57916)

Joel Lobb (NMLS#57916)

Senior Loan OfficerAmerican Mortgage Solutions, Inc.10602 Timberwood Circle Suite 3

#fhaloans #fhaloan #fha #conventionalloans #conventionalmortgage #kentuckymortgage #louisville #mortgage #homeloan #firsttimehomebuyers #khcloan #fhaloanky

#mortgagebroker #mortgagelender #homeloan

Kentucky FHA Loans in the State of Kentucky for 2022

FHA insured loan first time home buyer

Advantages of Kentucky FHA Mortgage Loans

- You can often make a down payment as low as 3.5 percent down to a 580 credit score

- You can finance a home with a 500 credit score with 10% down payment.

- Kentucky FHA loans are assumable meaning that if you have a good rate on your current mortgage and the potential buyer of your home meets FHA guidelines, then he can assume your low rate mortgage

- Kentucky FHA loans offer streamline refinancing without credit score minimums, verification of income, and no appraisals to refinance to a lower rate making it easier to qualify.

- Kentucky FHA loans offer flexible terms when it comes to previous bankruptcy or foreclosures. 2 years removed from Chapter 7 with reestablished

- credit, or if a Chapter 13, one year in the payment plan is eligible for FHA financing.

- Foreclosures on a past home. FHA will finance a home 3 years removed from the sale date of your foreclosure property

- 30 year fixed rate mortgage with usually the best going rates on government insured loans like FHA, VA, USDA etc.

- No prepayment penalty on Kentucky FHA loans.

- Higher debt to income ratio requirements when compared to Conventional loans because most Fannie Mae Conventional loans cannot have a higher debt to income ratio than 45% on the back-end

- You can make an FHA loan anywhere in the state of Kentucky with no geographical restrictions.

- Will allow for down payment assistance and grants for borrowers minimum down payments in the State of Kentucky through the likes of KHC, Welcome Home Grant, and Kentucky Housing Down Payment Second Mortgage loans.

- Kentucky FHA loans allow for unoccupied cosigner. For example, lets say you have a daughter that is getting ready to graduate college and does not have the income or credit history established yet to buy a home. FHA allows a family-member to co-sign for them to buy a home and you don’t have to occupy as primary residence. Note, FHA co-singers are not allowed to makeup for some that has bad credit, because they will take the lowest credit scores of both applicants. FHA usually allows for co-singers lack of income purposes only.

- Can usually close within 30 days just like a regular conventional mortgage. No extra time to close an FHA loan in Kentucky versus other secondary market loans like VA, USDA, Fannie Mae.

- You can use the FHA loan over and over. You can actually have two FHA loans open at the same time, but it gets tricky on this. Call or text me with more info if you have an FHA loan currently and would like to use FHA Financing again.

- FHA loans aren’t just for first time home buyers in Kentucky.

Disadvantages of Kentucky FHA Mortgage Loans

- There are loan limits in the State of Kentucky on FHA Mortgage loans. The maximum FHA loan in the state of Kentucky is $$420,680 for 2022. So if you were needing to finance a loan over this amount, you would need to look at doing a Conventional loan with the updated 2021 Kentucky State Loan Limits for a Fannie Mae loan being $647,250

- If buying a condo in Kentucky, FHA requires the condo development be FHA approved. There is a >>>list here of Kentucky FHA approved condos here.

- Seller must have own the home for 90 days before you can make an offer on the home. This comes into play where the seller bought the home as an investor and rehabbed the property and wants to sell for a quick profit. FHA mandates seller must maintain for 90 days before you can write up an offer on it. Also called FHA Flipping Policy. Read more here

- There is mortgage insurance. This is one of the biggest disadvantages for FHA loans. But as I tell most people, nobody rarely has a loan for 30 years, so if it meets your payment and your cash to close requirement, I tell people to go with it because it can be refinanced down the road and you are getting one of the lowers 30 year fixed rates out there. Both upfront and monthly mortgage insurance premiums you have to pay HUD/FHA. These premiums change whenever FHA/HUD replenish their insurance pool to pay claims from defaults, but currently the FHA upfront mortgage insurance premium is 1.75% and monthly is .85% and .80% of the loan amount. If you happen do a 15 year term or shorter, the mortgage insurance is cheaper monthly with .45 and .70 respectively each month. The upfront mortgage insurance is the same for a 30 year and 15 year at 1.75%

- FHA Mortgage insurance can be on the loan for life of loan. This is a recent change made in 2016 when FHA lowered there premiums for upfront and monthly mi premiums, but made the mortgage insurance for life of loan for some FHA loans.

- If you put down more than 10% on the loan, or have at least 10% equity in the home for a refinance, you only have to pay mortgage insurance for 11 years before it automatically falls off.

- Obviously you can refinance out of an FHA loan at anytime, since it does not a prepayment penalty, and you can potentially get a refund of your upfront mortgage insurance if paid off within 3 years on sliding scale.

-

I have incorporated some charts below to illustrate the different Kentucky FHA Mortgage Insurance premiums to explain it better.

-

The upfront mortgage insurance is usually financed into the loan, so it will look like you are borrowing more than the standard 3.5% down payment because this is financed into the loan. Some borrowers elect to pay it out of pocket upfront, but I have never seen this done in my 20 years of doing FHA loans in the State of Kentucky

- Kentucky FHA Loans Greater Than 15 Years MIP Chart

- 👇

Base Loan Amt. LTV Annual MIP ≤$625,500 ≤95.00% 80 bps (0.80%) ≤$625,500 >95.00% 85 bps (0.85%) >$625,500 ≤95.00% 100 bps (1.00%) >$625,500 >95.00% 105 bps (1.05%)

Kentucky FHA Loans Less Than or Equal to 15 Years MIP Chart👇

Base Loan Amt. LTV Annual MIP ≤$625,500 ≤90.00% 45 bps (0.45%) ≤$625,500 >90.00% 70 bps (0.70%) >$625,500 ≤78.00% 45 bps (0.45%) >$625,500 78.01% – 90.00% 70 bps (0.70%) >$625,500 >90.00% 95 bps (0.95%) When can I get the FHA mortgage insurance off my Mortgage Loan? See chart below 👇👇

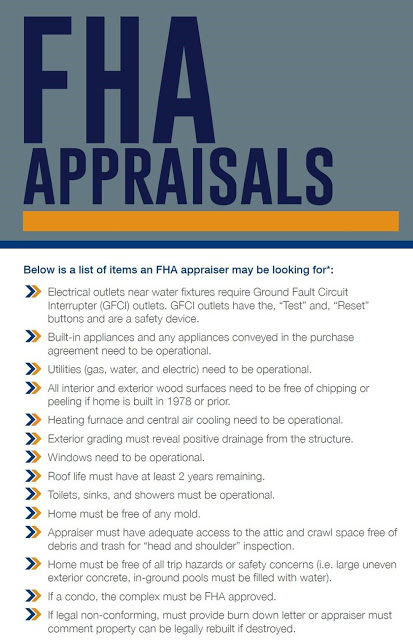

- Appraisals. On an FHA appraisal, the FHA appraiser has to turn on the utilities to make sure they are in worked order when he gets there. This is different that Conventional loan appraisals. A lot of realtors or buyers think that FHA loans are harder due to appraisals, but honestly, they’re really not. FHA puts these minimum HUD standards in place to make sure the home is in good working order and SAFE to live in. I.e.is there any lead based paint or chipping paint that could lead to poisoning It is all about Safety with FHA and HUD on these appraisals. The value is determined just like a regular Conventional, USDA, VA appraisals whereas they compare the house to 3 recent homes sold in the area to get a value.

- Some lenders don’t offer FHA loans due to their complexity and sale on the secondary market, so if you call a local lender in Kentucky and they don’t offer FHA loans, the reason is usually they don’t have the team in place to do them or don’t want to do them due to lack of experience on the secondary government market.

- Government Liens. FHA will not be an option for you usually if you have unpaid federal tax liens, delinquency on federal backed-government loans, or a claim with social security etc. FHA loans are ran through aCAVIRS alert system to check to see if you are delinquent on any federal oblation. If so, this swill stop you until you can clear the CAVIRS alert system. For example, I did a loan for a buyer that had a delinquent federal debt with his student loan that happened over 14 years old. It was off the credit report and title search, so I had to switch to a conventional loan to make the home loan work.

- FHA loans are not good for second homes or investment properties. FHA loans are mainly for single family residence 1-4 unit, that are going to occupied primarily as main home.

In summary, FHA loans have few drawbacks other than the mortgage insurance in my opinion. It is a great first time home buyer program or borrowers with past credit problems to get into a house of their own with very little out of pocket, at a low 30 year fixed rate, and no prepayment penalty

Questions about qualifying for a FHA loan in Kentucky . Give me text, call or email below. Love to help you out on your next home or refinance in Kentucky

Read more below about specific FHA Loans in Kentucky.👇👇👇

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Louisville Kentucky Mortgage Broker Offering FHA, VA, USDA, Conventional, and KHC Zero Down Payment Home Loans | October 17, 2018 at 3:54 pm | Tags: fha gift funds, fha loan kentucky, FHA Loans Kentucky Housing First time home buyer, fha mortgage, fha mortgage loan, gift funds for fha mortgage, kentucky fha loans |

Louisville Kentucky Mortgage Rates for First Time Home Buyers

Do I qualify as a Kentucky first-time home buyer?

You are typically considered eligible to apply for first-time home buyer loans and benefits if you haven’t owned your principal residence within the past three years.

Some first-time home buyer assistance programs are even more lenient, offering financial aid in specific areas targeted for redevelopment, even to repeat buyers.

Kentucky First-time home buyer benefits

Benefits can include low- or no-down-payment loans, grants or forgivable loans for closing costs and down payment assistance, as well as federal tax credits with the Kentucky Housing Agency or KHC

Is there an income limit to qualify as a first-time home buyer?

Income limits come into play when you are applying for local, state or federal government assistance. Some national mortgage programs, such as loans issued or backed by the U.S. Department of Agriculture, also have household income limits.

Some low-down-payment conventional loans do, too.

In these cases, your income may be benchmarked to local county limits for low- and moderate-income households.

Lenders, even those working with loan programs authorized by a state housing agency, will likely consider your debt-to-income ratio when determining if you qualify.

How to qualify for a first-time home buyer grant

Grants or forgivable loans that typically don’t require repayment are available to low- and moderate-income borrowers through state first-time home buyer programs. Approval standards vary by program and location but often include household income and home sale price limits.

How to qualify for down payment assistance

Just as for grants, down payment and closing cost assistance is often offered by local and state housing authorities. Again, qualifications vary. Look for income and home sale price caps here, too.

Don’t be surprised if a first-time home buyer class is required to qualify for a grant or down payment assistance. These classes are designed to help you navigate the homebuying process, and can be a good idea to take whether they’re mandatory or not.

What are the requirements to qualify for a first-time home buyer loan?

Qualifications required for approval of a loan vary by the type of mortgage — and even by the lender — but here are some general guidelines:

Kentucky Conventional loans:

For a 3% down payment, you’ll need at least a 620 FICO and a debt-to-income ratio below 50%. The higher your credit score or the lower your debt, the better your chances are for approval.

Kentucky FHA loans:

If you want a down payment as low as 3.5%, you’ll need a FICO score of 580 or higher. With 10% down, your required credit score may go as low as 500.

Kentucky VA loans:

Down payments aren’t generally required for a loan backed by the Department of Veterans Affairs. And while VA-backed loans don’t have a minimum FICO score as a part of their official requirements, many lenders look for a score of 620 or better.

KentukcyUSDA loans:

Another no-down-payment option, USDA-backed loans are typically issued for rural or suburban properties. Income limits apply. A FICO score of 640 or better is generally required, though exceptions with documentation can allow a lower score.

Lenders can add additional conditions, called “overlays,” to loan approval. This is another good reason to shop for more than one lender.

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com