When it comes to buying a home in Kentucky, FHA loans are a popular choice for many first-time homebuyers due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know: Understanding these … Continue reading “Qualifying for an FHA Loan in Kentucky”

When it comes to buying a home in Kentucky, FHA loans are a popular choice for many first-time homebuyers due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

Credit Score Requirements:

FHA loans are known for accommodating borrowers with lower credit scores. While the minimum required credit score can vary, typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. However, borrowers with credit scores between 500 and 579 may still be eligible with a higher down payment, usually around 10%.

Down Payment:

The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

Work History:

Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history, preferably with the same employer or within the same field, helps demonstrate financial stability and the ability to repay the loan.

Debt-to-Income Ratio (DTI):

The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income and can go higher up to 56% with good credit scores, large down payment or shorter term loan although lenders may consider higher ratios in certain cases if compensating factors are present.

Bankruptcy and Foreclosure:

FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

Mortgage Term:

FHA loans offer various mortgage term options, including 15-year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

Occupancy: Primary residences not for rental properties

Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

can be used for refinances, not only for purchases.

Max FHA loan in Kentucky is $498,257. This changes every year

No income limits nor property restrictions on where home is located

Can close within 30 days typically with good appraisal and title work

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can also provide valuable guidance and assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

This content provides detailed information about Kentucky mortgage loan options, credit score requirements, and tips for improving credit scores. It covers FHA loan requirements, credit bureau scores, credit utilization, and factors affecting mortgage approval. The post emphasizes the importance of credit history and offers specific advice for maintaining a favorable credit profile to qualify for a mortgage in Kentucky.

The Best Kentucky Mortgage Loan Options When Looking for your first house in Kentucky Kentucky First-time Home Buyer Programs👀💯👇‼

Kentucky Mortgage Requirements for FHA, VA, USDA and Fannie Mae

FHA loan in Kentucky you will be confronted with minimum credit score requirements set forth by FHA and the lender. Even though FHA will insure the mortgage loan at a certain credit score, you will see that lenders will create “credit-overlays” to protect their risk and ask for a higher credit score.

So keep in mind when you are getting an FHA lenders will have higher credit score minimums in addition to the FHA Mortgage Insurance program.

For a Kentucky Homebuyer wanting to purchase a home or refinance their existing FHA loan, FHA requires a 3.5% down payment and the borrower must have a 580 FICO Credit Score. If the score is below 580, then you would need 10% down and still qualify on a manual underwrite.

You must have a FICO score of at least 500 to be eligible for a Kentucky FHA loan. If your FICO score is from 500 to 579, your down payment on the loan is 10 percent of the loan.

If your FICO score is 580 or higher, your down payment is only 3.5 percent. If your credit score is less than 580, it may be more cost-effective to take the necessary steps to improve your score before taking out the loan, rather than putting the money into a larger down payment.

How do they get the credit score: There are three main credit bureaus in the US. Equifax, Experian, and Transunion. The three scores vary but should be relatively close as long as the same creditors are reporting to the same bureaus.

You will get a variation in the scores due to all creditors or collection companies don’t report to all three bureaus. This is why they take the mid score. So if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying credit score would be 620

Based on my experience with lenders that I deal with in Kentucky on FHA loans, most lenders require 620 middle credit score for consideration for loan approval.

How do they get the score: They take the mid score, so if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying score would be 620.

If your score is below 620, a manual underwrite is where the AUS (Automated Underwriting System) refers your loan to a human being, and they look at the entire file to see if they can overturn and approve the mortgage loan because the Desktop Underwriting Automated Software could not approve you.

With scores below 620, they typically will want to verify your rent history, have no bankruptcies in the last two years, and no foreclosures in the last 3 years.

If you have had any lates since the bankruptcy this will probably result in a denial on a refer manual underwrite file.

Your max house payment will be set at 31% of your gross monthly income, and your new house payment plus the bills you are paying on the credit report cannot be more than 43%.

Typically, on scores below 620 for FHA loans, they will also look at reserves or money you have saved up after the loan is made to try and qualify you. For example, if you have a 401k or savings account that has at least 4 months reserves (take your mortgage payment x 4) and this would equal your reserves. They look at this as a rainy day fund and could help you keep up on your bills if you were unemployed or could not work.

If you are looking to take a FHA loan in 2022 to buy or refinance a home in Kentucky, please contact me below with your questions about the credit score requirements and how they affect your loan approval.

The first thing to keep in mind is that qualifying for a mortgage involves a lot more than just a credit score. While your FICO score is a very important ingredient, it is just one factor. Lenders also look at your income and level of debt, among other things.

A FICO score between 600 and 640 is considered fair to good credit. But keep in mind, this range of credit scores does not guarantee you will qualify for a mortgage, and if you do qualify, it won’t get you the lowest interest rate possible. Still, to buy a home aim for a score of at least 620, recognizing that other factors weigh in the decision and that some banks may require a higher score.

What credit score do you need to get a low rate mortgage?

It uses to be that a score of about 720 would yield the lowest mortgage rates available. Today, the best rates kick in with a FICO score of 760. And interest rates go up significantly as your credit score drops. To give you an idea, the following table shows current rates by credit score and calculates a monthly principal and interest payment based on a $300,000 loan:

lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Transunion, Equifax, and Experian. The lenders will throw out the high and low scores and take the “middle score.” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614.

So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores.

Lastly, lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough.

offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores,

If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans.

The lenders I currently deal with have the following fico cutoffs for credit scores:

As you can see, different government-backed loan programs have different minimum score requirements with most lenders for an FHA, VA, or Fannie Mae loan, and 620 is required for the no down payment programs offered by USDA and KHC in Kentucky for First Time Home Buyers wanting to go no money down.

By paying down your credit card balances (credit utilization) and having a good pay history (payment history) ,this is the best way to raise your score.

The credit bureaus don’t update immediately, so I would not add to the balance or open any new bills or have any other lender do an inquiry on your credit report while we wait for the scores to hopefully go up in the next 30 days. Try to keep everything status quo and make your payments on time and keep your balances low or lower than what is now reporting on the credit report.

How to improve your credit score!

Pay Every Single Bill on Time, or Early, Every Month

Please understand one thing; paying your bills on time each month is the single most important thing you can do to increase your credit scores.

Depending on the credit bureau, there are 4 or 5 main items that determine everyone’s credit score. Of those items, your history of paying bills makes up about 35% of the score. THIS IS HUGE!

Paying your bills on time shows lenders that you are responsible. It will also spare you from paying late fees whether it is a charge from a credit card or an added fee from your landlord.

Use a calendar, or a phone app, or some other organized system to make sure that you pay your bills on time every single month.

Another big factor in calculating a credit score is the amount of credit card debt. Credit bureaus look at two things when analyzing your credit cards.

First, they look at your available credit limit. Second, they look at the existing balance on each card. From these two figures an available ratio is developed. As the ratio goes higher, so too will your credit score increase.

Here is one simple example. Suppose a person has the following credit cards, corresponding balances, and credit limits

Credit Card

Current Balance

Credit Limit

Chase Visa

$105

$1,000

MarterCard from local bank

$236

$1,500

BP MasterCard

$87

$500

Totals

$428

$3,000

From these numbers, we get the following calculation

$428/$3,000 = 14%

In other words, the person is using 14% of their available credit and they have 86% available credit. The closer that ratio is to 100%, the better the credit score will be.

MAIN TIP: Keep all credit card balances as low as possible.In this particular example, if they had a problem with their car, or needed medical attention or some other emergency, the person would have the money necessary to handle the situation without incurring new debt. This is wise on the consumer’s part and lenders like to see this kind of money management.

Credit Cards Part 2: 1 or 2 is Better Than a Wallet Full

The previous example showed a person that utilized just three credit cards. This is much better than someone who has 5+ credit cards, all with available balances. Why? Lenders do not like to see someone that has the potential to get too far in debt in a short amount of time.

Some people have 5, 10 or more credit cards and they use many of them. This shows a lack of restraint and control. It is much better, and neater, to have only 2 or 3 cards with low rates that handle all of your transactions. A lower number of cards are easier to manage and it does not give a person the temptation to go on a huge shopping spree that could take years to payoff.

MAIN TIP: Try to limit yourself to no more than 2-3 credit cards.

Keep the Good Stuff Right Where it is

Too many people make the mistake of paying off old debts, such as old credit cards, and then closing the account. This is actually a bad idea.

A small part of the credit score is based on the length of time a person has had credit. If you have a couple of credit cards with a long track history of making payments on time and keeping the balance at a manageable level, it is a bad idea to close out the card.

Similarly, if you have been paying on a car or motorcycle for a long time, do not be in a hurry to pay off the balance. Continue to make the payments like clockwork each month.

An account that has a good record will help your scores. An account that has a good record and multiple years of use will have an even better impact on your score.

MAIN TIP: Keep old accounts open if you have a good payment history with them.

Stop Filling Out Credit Applications

Multiple credit inquiries in a short amount of time can really hurt your credit scores. Lenders view the various inquiries as someone that is desperate and possibly on the verge of making a bad financial choice.Too many people make the mistake of getting more credit after they are approved for a loan. For example, if someone is approved for a new credit card, they feel good about their finances and decide to apply for credit with a local furniture store. If they get approved for the new furniture, they may decide to upgrade their car. This requires yet another loan. They are surprised to learn that their credit score has dropped and the interest rate on the new car loan will be much higher. What happened?

If you currently have 2 or 3 credit cards along with either a car loan or a student loan, don’t apply for any more debt. Make sure the payments on your current debt are all up to date and focus on paying them all down.

In a few months of making timely payments your scores should noticeably go up.

MAIN TIP: Limit your new loans as much as possible

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

This content discusses the credit score requirements, down payment options, and mortgage insurance for Kentucky Conventional and FHA Loans. It also outlines bankruptcy timelines for eligibility and provides contact information for Joel Lobb, a Senior Loan Officer. The disclaimer emphasizes that loan approvals are subject to various qualifications and conditions, and the content is not endorsed by any government agency.

Kentucky FHA Loans are good for borrowers who have the following:

• Credit scores less than 680.

• Less than 5% down payment and no reserves to use.

• Borrowers with past foreclosures between 3 and 7 years old.

• Borrowers with past short sales between 2 and 4 years old.

• Borrowers who need a gift for the down payment and/or closing costs, prepaid taxes and

insurance.

The FHA Mortgage Insurance premium is a premium that exists for the FHA Loan that is

paid up front and monthly by the homebuyer. This premium protects the lender should the

buyer default. They vary per state and per type of loan Kentucky home buyers qualify for. In Kentucky, upfront mortgage insurance premiums are 1.75%.

Below are the rates per type of loan:

• 15-Year Fixed with down payment more than 10%: .45%

• 15-Year Fixed with down payment less than 10%: .70%

• 30-Year Fixed with down payment more than 5%: .80%

• 30-Year Fixed with down payment less than 5%: .85%

Kentucky Conventional loans are usually reserved for the following:

• Credit scores greater than 680

• Greater than or equal to 5% down payment with reserves

• Borrowers with past foreclosures over 7 years old.

• Borrowers with past short sales between 5-7 years old.

• Borrowers who have a lot of money saved up and want to get rid of mortgage insurance within the first 5 years give or take. 20% equity position is needed for no mi

Advertisement

The biggest difference between conventional loans and FHA loans comes down to the mortgage insurance. Mortgage insurance is more expensive for FHA loans, but the trade off is a lower fixed rate than conventional loans.

On Conventional loans there is no upfront mortgage insurance like FHA, and if you have a high credit score you can possibly get a lower monthly mi premium as compared to FHA where everybody gets the same mortgage insurance premium not matter your credit score or down payment.

Lastly, FHA Mortgage insurance is for life of loan, whereas Conventional mortgage insurance or pmi it’s called, is discontinued once you reach the 80% threshold equity position of your home loan.

Again, I would not get too caught in FHA having mortgage insurance for life of loan, because most loans are only kept open a minimum of 5-7 years so a lot of times it may make sense to go with the lower rate and pay the mortgage insurance with FHA because most people don’t hold their mortgage for 30 years.

You can call or text me with your questions and we can compare the differences based on your credit score, down payment and income.

Equal Housing Lender. NMLS#:57916 http://www.nmlsconsumeraccess.org/Rates, terms, and program information are subject to change without notice. Subject to certain approvals, terms and conditions. This is not a commitment to lend.

Not part of any government lending agency and only lending in the State of Kentucky.

Looking at FHA loans vs Conventional loans can arm you with a lot of valuable information as these are the 2 most popular mortgage loan products today. Before getting to the content let’s look at some abbreviations that will need to be defined.

PMI stands for Private Mortgage Insurance

MIP stands for Mortgage Insurance Premium

Credit Scores are a numerical measure of your credit worthiness, the maximum score is 850

Debt-to-Income Ratio measures your monthly income versus your monthly obligations. A good rule of thumb is to try to be below 45%

FHA Loans vs Conventional Loans

Conventional Mortgage Benefits

20% down payment preferred to avoid PMI

No upfront PMI

3% Down Payment Conventional Loan Option is available

PMI expires once principal balance is less than 78%

Houses do not have to be owner-occupied (so they can be used at rentals)

Can purchase any condominium and townhome (no FHA regulations)

Conventional Mortgage Disadvantages

Significant upfront investment (20% down preferred)

Credit score of 620 required

No Down Payment Assistance

Down Payment must be at least 5% unless you qualify for a 3% conventional mortgage

Harder to Qualify for a Conventional Mortgage

No government inspection so the home can be in any quality

Only a portion of a down payment can be a gift

Interest rates are higher than FHA loans

Most of the disadvantages of conventional mortgages stem around qualifications and resources needed upfront. If a borrower has significant resources most of these disadvantages are of little consequence.

The major advantage to going with an FHA loan is that there are much more lax credit standards you have to meet to obtain financing. Usually, FHA mortgages require a lower down payment, can work with lower credit scores, less elapsed time is needed if you have some credit problems (charge-offs, foreclosures) and you can use a non-occupant co-borrower or co-signer (who is a relative) to help you qualify for the loan. That way you can use blended ratios. Blended ratios are debt-to-income ratios that equally blend or combine the primary borrower’s income and the non-occupant co-borrower’s income and monthly payments to help get approval for the loan. Except for HomeReady (formerly Fannie Mae HomePath) mortgages, conventional loans do not allow you to use a non-occupant co-borrower.

Government-backed program. Ideal for first-time home buyers

Easier to obtain, lower credit scores needed and lower minimum down payment

Down Payment minimum is 3.5%

All of down payment can be a gift

Down Payment Assistance Available (in some circumstances)

No reserves required

Minimum credit score is 500 (for 3.5% down payment)

edition to be approved for FHA so there are less potential upfront repairs needed

Lower interest rates than conventional mortgages

FHA Loan Disadvantages

FHA loans require the owners to live in the home

Mortgage Insurance Premium required if borrowers put down less than 10%

Private Mortgage Insurance monthly cost is higher for FHA loans

Government Licensed Inspector required to inspect home before sale can be approved

Condominiums require FHA approval

FHA Loans take longer to process because of government requirements and all mandated repairs have to be completed before sales can be finalized

Most of these disadvantages involve extra requirements or limits added to the process of the house (see Pros and Cons of FHA Loans). Some of these might not be disadvantages depending on one’s personal situation, but they are extra steps to note. Since FHA mortgages are a government program, more care and consideration goes into the process, which may be better in some situations.

FHA loans vs Conventional loans

There are four important numbers in deciding which loan you will go with: credit scores, down payment amount, debt-to-income, and mortgage insurance percentage rate. Conventional mortgages and FHA home loans have different limits and rates which are important to examine. They also have important differences which affect the availability of properties, the condition of the properties one wishes to buy and how your down payment can be paid. So comparing FHA loans vs Conventional loans can sometimes be a tricky endeavor.

Down Payment Requirements

Conventional Mortgages require between 5 and 20% upfront

In certain circumstances, down payments can be as low as 3% (Conventional 97 loan program)

FHA Mortgages have 2 possibilities

If Credit Score is 500-579 then 10% down payment is required (not all lenders will even go down this low)

If Credit Score is 580+ then 3.5% down payment is required

Debt-to-Income Ratio

Conventional Mortgages’ maximum debt-to-income ratio is 43% (hard cap)

FHA Mortgages’ maximum debt-to-income ratio is 45%

Soft cap as in certain circumstances this can be adjusted up to 50%

Mortgage Insurance Premium Rates

FHA Mortgages

If Down Payment is 10% or more the percentage is .80% MIP

If Down Payment is less than 10% the rate is .85% MIP.

Credit Score Minimum Requirement

Conventional Mortgage minimum credit score

Most lenders will require between 620 and 640

Some lenders it will be as high as 700

FHA Mortgage minimum credit score

Credit Score is a minimum of 500 if putting 10% down

Credit Score is a minimum of 580 if not

These four numbers are important to know and will affect one’s decision to pursue a particular type of home loan. Knowing your combination of numbers as you are looking to buy a house will help buyers find the best loans for their particular situation.

OTHER COMPARISONS

All sellers will take conventional mortgages and some sellers will not take FHA Loans

People looking for short-sells won’t take FHA because FHA has a longer closing process.

If sellers know there are FHA repairs that are needed in order to sell their house, they will not always accept FHA financing.

Thus, if one is wanting a low-risk transaction then the FHA home loan route is a better option to pursue, even though it limits your options for homes that you might wish to buy. If one is looking to fix-up a house and raise its equity quickly then a conventional loan is going to be more beneficial because there are no requirements as to the condition of the house and it’s occupied status.

DOWN PAYMENT GIFTING

Making the Down Payments (Assistance and Gifts)

Conventional mortgages have no assistance but can be partially fulfilled with a gift

FHA Mortgages have loans and assistance programs available and the whole down payment can be fulfilled with a gift

In this article, we have given you the basic parameters of FHA loans vs Conventional loans. The conventional loans are for people who have a better financial track record and can handle a larger upfront cost. Because of PMI, conventional loans are cheaper in the long run if you can put enough of a down payment to get rid of PMI. However, there are no down payment assistance programs to help you reach that goal. FHA loans are for people who are looking to build their investment and in some cases may not have a great financial track record. FHA loans have lower down payment requirements and many grants/forgivable loans to help people wanting to buy a first house in which to live for at least a few years. It is important to assess your situation and decide which mortgage is going to work better for your circumstances.

CONCLUSION

Both mortgages have a lot of benefits and drawbacks because they are designed for people with different needs. This article has hopefully helped you to get a basic understanding of the different terms and conditions of different mortgage packages when looking at FHA loans vs Conventional loans. Home buying can be an emotional roller coaster and the knowledge in this article will help you navigate the various emotional struggles of home buying.

How to Qualify for a Kentucky FHA Mortgage Loan with a lender in Kentucky?

The requirements for Kentucky FHA loans are set by HUD.

Borrowers must have a steady employment history of the last two years within the same industry or line of work. Recent college graduates can use their transcripts to supplant the 2-year work history rule as long as it makes sense.

Self-Employed will need a 2-year history of tax returns filed with IRS. They will take a 2-year average.

FHA requires a 3.5% down payment. Can be gifted from a family member or from a retirement savings plan, or money saved up. Any type of cash deposits is not allowed for down payments. No exceptions to this rule!! This is one of the biggest issues I see in FHA underwriting nowadays.

FHA loans are for primary residence occupancy. Not rental houses.

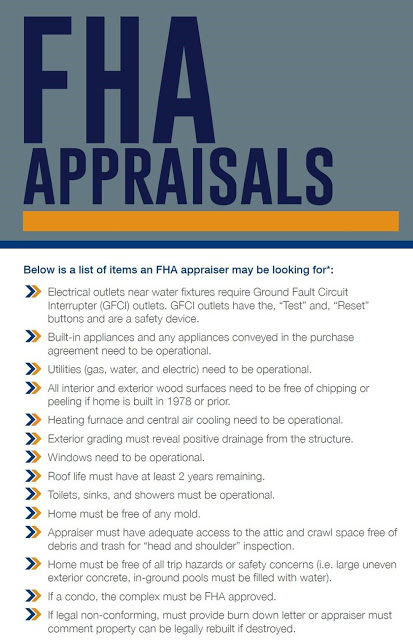

Borrowers must have a property appraisal from an FHA-approved appraiser.

Borrowers’ front-end ratio (mortgage payment plus HOA fees, property taxes, mortgage insurance, homeowners insurance) needs to be less than 31 percent of their gross income, typically. You may be able to get approved with as high a percentage as 43 percent. If the Automated Underwriting System gives you an Approved Eligible you can go higher on the debt ratios

Borrowers must have a minimum credit score of 580 for maximum financing with a 3.5% down payment

Borrowers must have a minimum credit score of 500-579 for maximum LTV of 90 percent with a minimum down payment of 10 percent. Most lenders will not go below 580 to 620 score, and very few lenders will go to 580 score. It’s best to work on getting your scores up before you apply or work with a loan officer to improve them.

2 years removed from Chapter 7 is required with good pay history after bankruptcy

1 year removed from Chapter 13 is okay with an excellent pay history with the Chapter 13 plan and permission from the trustee. You will need to qualify with the Chapter 13 payment along with a new house payment. Again, scores will play into your loan pre-approval.

Typically borrowers must be three years out of foreclosure and have re-established good credit. Exceptions can be made if there were extenuating circumstances and you’ve improved your credit. If you were unable to sell your home because you had to move to a new area, this does not qualify as an exception to the three-year foreclosure guideline.

The property must be safe, sound and secure, in compliance with minimum property standards as defined by the U.S. Department of Housing and Urban Development, or HUD.

You may not have delinquent federal debt or judgments, or debt associated with past FHA loans. Caivrs Alert System will show up if you owe the government money.

Why Lenders Use CAIVRS

It is true that your CAIVRS report can help lenders to predict the risk of doing business with you, just like a traditional consumer credit report. But the primary reason lenders check your CAIVRS report is because they are generally required to do so for any applications that involve a federal loan (FHA, VA, USDA, SBA, etc.). Lenders are required to conduct a CAIVRS search because of Title 31 of the United States Code (Section 3720B) bars “delinquent federal debtors from obtaining federal loans or loan insurance guarantees.”

Kentucky FHA Loan Requirements for 2024

Gift Rules for Down-Payment Sources Guidelines on FHA Mortgage Programs

One of the biggest obstacles to buying a home for Americans is the down payment. There was a time when you needed a 20% down payment and a high credit score to buy a home. But in 2022, you can buy a home with average to below-average credit and low down payment in some cases. One of the most popular loan programs for these buyers if the FHA loan. A major advantage of the FHA mortgage loan is you can get approved with only a 3.5% down payment with a 580 or higher credit score. If you have a lower score than that, you need a 10% down payment.

Still, there are situations where the borrower is having trouble coming up with the down payment for the loan. What to do then? FHA guidelines do allow other options. Keep reading to learn more.

More on FHA Down Payments and Approved Sources

As we noted above, you are required to have at least a 3.5% down payment to be approved for an FHA loan. The money must be verified by the FHA-approved lender to come from an ‘approved source.’ What is an approved source, anyway? Most people get their down payment from cash reserves, investments, borrow from 401k or IRA, etc. The idea behind verifying where the money came from is to make sure the borrower did not get the down payment from a credit card or payday loan, etc.

But there are other options for your down payment. The funds also can come from a gift. The gift and the giver do need to meet FHA requirements, but this flexible guideline makes it possible to get into an FHA loan with, technically, zero money down. To determine if the down payment gift can be used or not, it is necessary to check HUD rules. According to HUD 41.55.1 Chapter 5 Section B, for the funds to be a gift, there cannot be any expected repayment of the money.

Also, FHA will scrutinize the giver of the gift. Chapter 5 of the HUD Code states the cash gift is OK if it comes from your relative; employer or labor union; close friend with a defined interest in you; charitable organization; government agency or public entity.

FHA also states who cannot give gift funds to you for the down payment. These are the seller; the real estate agent or broker on the deal; the builder or an associated entity.

Gift Terms Explained

The gift for your down payment cannot be made based upon paying it back later. You are required to get a gift letter from the person or organization. The letter should state that you are not required to pay the money back. It also should provide the contact information for the borrower, such as name, address, and phone number. Also included should be the bank account from which the funds will be sent.

The gift donor should be OK with giving a bank statement with the letter. Also, he or she should ensure that the transfer amount matches what is in the gift letter and what is deposited into your account.

FHA rules are very specific on these areas to ensure that the home buying process through FHA is fair and just. But as long as you follow the FHA rules, you should be able to get help with your down payment from a friend or relative.

Don’t Have Friends or Family Who Can Help?

Not every borrower has friends or family who can give them a gift for their down payment. But HUD lists many government programs spread throughout the country in most states that can offer down payment and closing cost help for certain borrowers.

It also is worth checking if your employer and state have employer-assisted housing. This program can help people with moderate incomes to get a loan to cover closing costs and down payment. Look up FHA in your state on Google to see what is available.

The FHA is actually not the lender. They insure the loans that are issued by FHA-approved lenders. FHA loans are gear more toward borrower’s with less than 20% down payment and credit issues in the past.

Qualifying for a FHA Loan Mortgage In Kentucky

Credit Scores and Down Payment Percentages – Each year, the rules for qualifying for these loans changes. For 2024, applicants need a minimum credit score of 580 in order to get the low down payment, which is 3.5 percent.

For those whose credit score is less than 580, they will have to come up with 10 percent for their down payment. This does not guaranteed a mortgage loan approval if you have the certain credit scores, just a the minimum required.

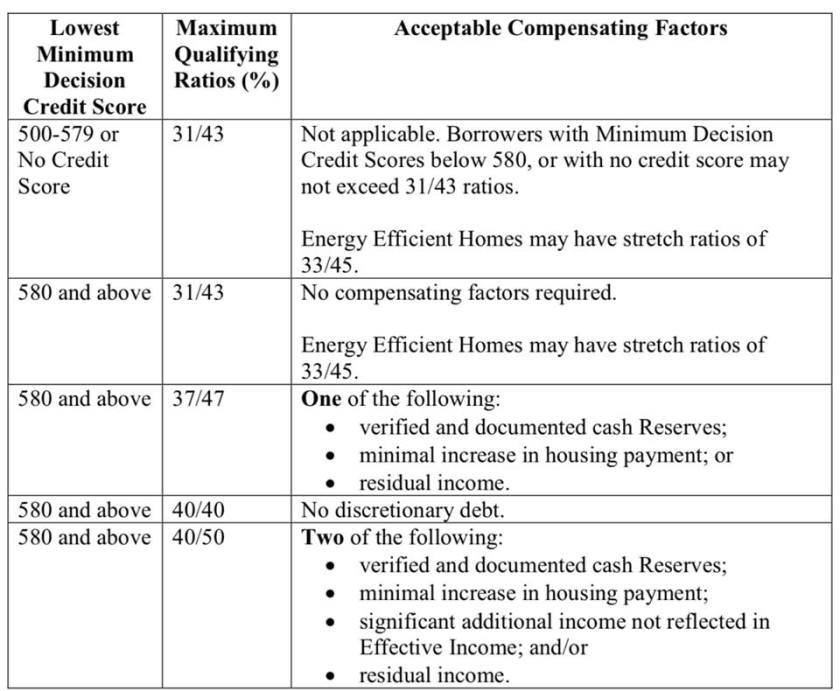

Compensating Factors for FHA loan Approval

The credit score is just one part of the story. The FHA will also evaluate the borrower’s bankruptcies, foreclosures, prior payment history on other debts. They will also want information on difficulties that kept the borrower from making payments on other debts in the past.

Negative strikes against qualifying for the loan include not having any credit history or a bankruptcy.

Someone with a bankruptcy will have to wait for two or more years after their bankruptcy before applying for an FHA-insured loan.

If you have late payments on debt obligations, it is best to wait until you have had a full year of on-time payments before you apply for a FHA-insured loan.

If you have had a foreclosure in the past, you may still be able to get a FHA-insured loan three years after your foreclosure. The lender will be looking at the circumstances behind the foreclosure.

If you have had any civil judgement against you for money owed, collections actions or unpaid/unresolved federal debt, the FHA-approved lender will be required by the FHA to establish that all of these outstanding issues are resolved or paid before you can go through closing.

Watch out for student loans if they are delinquent because sometime this can cause a lien against you in the form of a CAVIRS Alert with HUD

As you can see, many types of borrowers who would not be eligible for a traditional mortgage, or who would face exorbitant interest rates, will be able to qualify for a FHA-insured loan at attractive interest rates.

Your income has to be verifiable in some way, whether that be through pay stubs, your income tax returns. No bank statements or cash deposits , or undocumented income can be used for income qualifying purposes.

Debt-to-Income Ratio Requirements –

Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.

Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.

If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Property Requirements for a Kentucky FHA Loan

It must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.

It is really not too hard to pass FHA loans and the appraisal process.

Pros of FHA Loans –

New homebuyers and those who have lower credit scores or who have other blemishes on their credit history will often qualify for FHA-insured loans.

Even though these borrowers are considered “subprime” to a traditional lender, they will receive attractive interest rates through the FHA-insured mortgage programs.

The down payments required from borrowers are lower than those required by traditional mortgage lenders.

These loans can be combined with other forms of public assistance for lower income or new borrowers so that the borrower will not need to come up with a down payment of any kind.

Cons of FHA Loans –

Since the FHA is not actually the lender, and you have to go through FHA-approved lenders, you may not qualify due to stricter standards that the lender has for the loan.

Because you are not paying 20 percent as a down payment, the FHA requires two mortgage insurance premiums to be paid. One is an upfront premium that is 1.75 percent of the loan amount. Lenders often will allow you to make that mortgage insurance premium a part of your loan. The second is an annual mortgage insurance premium that is .45 percent or 1.05 percent. This premium is paid monthly.

What credit score do I need to qualify for a Kentucky FHA loan is one of the most common questions I hear from Kentucky homebuyers?

The short answer is you must have a minimum credit score of 500 to be eligible for an FHA loan in Kentucky. Anything lower than 500 disqualifies you from consideration for an FHA loan.

There are two sets of credit score requirements for a Kentucky FHA Loan

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default.

You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an Kentucky FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them.

This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

5 Things to Know about buying a house and getting a Mortgage Loan approval in Kentucky for 2023

1. Do Mortgage Rates Change Daily?

Just like the gas prices at the pump, mortgage rates can change daily or throughout the day. Typically mortgage rates are published at 10-11 am daily by most lenders and you can lock up through the close of business which is usually around 6-7 PM. Mortgage rates can change up or down throughout the day based on various financial, economics, and geopolitical news in the US Financial markets and World markets. Generally speaking, good economic news is bad for rates and vice versa, bad economic news is good for mortgage rates.

The good news is this: Once you find a home and get it under contract, you can lock your mortgage loan rate. Typically it takes about 30-45 days to close a mortgage loan in Kentucky, so the typical lock is for 30-60 days. If rates get better you may be able to negotiate a better rate with your lender, but they usually have to improve by at least 25 basis points (.25) to do that. Not all lenders offer this option. The longer you lock the loan, the greater the costs. It is usually free to lock in a loan for up to 90 days without having to pay a fee.

What a lot of lenders are experiencing now is that some loans don’t close on time for various reasons. You can always extend the lock on the loan but it will costs you usually .125 basis points to do so. If you let the lock expire on the loan, then you have to take worse case pricing on that day when you go to relock. It is usually best to extend the lock on your loan.

2. What kind of Credit Score Do I need to qualify?

When applying for a mortgage loan, lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Trans union, Equifax, and Experian. The lenders will throw out the high and low score and take the “middle score” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614. Most lenders will want at least two scores. So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores. Most lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough. The Secondary Market of Mortgage loans offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores, very few lenders will go below the 620 threshold. If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans. The lenders I currently deal with have the following fico cutoffs for credit scores: FHA–580 minimum score VA—-580 minimum score Fannie Mae–620 minimum score USDA–620 minimum score KHC with Down Payment Assistance –620 minimum score.

As you can see, 580-620 is the minimum score with most lenders for a FHA, VA, or Fannie Mae loan, is required for the no down payment programs offered by USDA for Kentucky for First Time Home Buyers wanting to go no money down.

3. What are the down payment requirements?

The most popular programs for Kentucky First Time Home Buyers usually involves one of the following housing programs outlined in bold below: FHA:

FHA will allow a home buyer to purchase a house with as little as 3.5% down. If your credit scores are low, say 680 and below, a lot of times it makes sense to go FHA because everyone pays the same mortgage insurance premiums no matter what your score is, and the down payment can be gifted to you. Meaning you really don’t have to have any skin into the game when it comes to down payment.

They even allow down payment assistance for down payment requirements of 3.5% through eligible parties like Kentucky Housing, Welcome Home Grants and Louisville KY and Covington Kentucky Down Payment Grants.

Lastly, FHA will allow for higher debt to income ratios with sometimes getting loan pre-approvals up to 55% of your total gross monthly income. So if you have a debt to income ratio of over 50%, Fannie Mae will not do the loan and USDA usually likes their debt to income ratios no more than 45%.

Think back to the last time you financed a purchase — be it a home, automobile, or what have you… You may remember having heard the term “debt-to-income ratio.” Today I want to spend some time going over exactly what this ratio is, and to also touch on how it can effect your personal finances.

4. What is your debt-to-income ratio?

Commonly referred to as your “DTI,” your debt-to-income ratio is a personal finance benchmark that relates your monthly debt payments to your monthly gross income. As an example… Let’s say that your gross monthly salary is $5,000 and you are spending $2,800 of it toward monthly debt payments. In that case, your DTI would be an unhealthy 56%. This version of your DTI is sometimes referred to as your “back-end” DTI. This is often broken down further to give a front-end debt-to-income ratio, which is a component of your back-end DTI.

How to calculate your front-end DTI for a Kentucky Mortgage Loan Approval

Your front-end DTI is calculated by dividing your monthly housing costs by your monthly gross income. Front-end DTI for renters is simply the amount paid in rent, whereas for homeowners it is the sum of mortgage principal, interest, property taxes, and home insurance (i.e., your PITI) divided by gross monthly income.

From above, if that $2,800 in debt payments is attributable to $1,500 in housing costs and $1,300 in non-housing costs, then your front-end DTI is $1,500/$5,000 = 30% (and your back-end ratio is still 56%, as calculated above). Fannie Mae: Fannie Mae requires just 3% down with their new Home Possible Program, but if you use their traditional mortgage loan, then 5% is the Fannie Mae Standard. Fannie Mae will go down 620 score, but if your scores are below 680, I would look seriously at the FHA loan program because Fannie Mae has steep increases to the interest rate and the mortgage insurance premiums if your scores are low. A couple of good things about Fannie Mae is that you can buy a larger priced home and have a large loan amount due to FHA only allowing most Kentucky Home Buyers a maximum mortgage loan amount of $356,000 for a max FHA loan and $545,000 for Fannie Mae Conventional loans in Kentucky for 2020. Lastly when it comes to mortgage insurance, FHA mortgage insurance premiums are for life of loan while Fannie Mae mortgage insurance premiums drop off when you develop 80% equity position in your house. But as a tell most people, nobody has a loan for 30 years, and the average mortgage is either refinanced or home sold within the first 5-7 years. VA Loans-

VA loans offer eligible Veterans and Active Duty Personnel to buy a home going no money down with no monthly mortgage insurance. This is probably the best no money down loan out there since the rates are traditionally very low on comparison to other government insured mortgages and no monthly mortgage insurance. The VA loan can be used anywhere in the state of Kentucky with the maximum VA loan limit being removed for 2021 USDA Loans-

USDA loans offer people buying a home in rural areas (typically towns of $20k or less) to buy a home going zero down. You cannot currently own another home and there is household income limits of $90,200 for a household family of four, and up to $119,300 for a household of five or more. You search USDA website for eligible areas and household income limits below at the yellow highlighted link :

KHC or Kentucky Housing- Kentucky First Time Home Buyers typically use KHC for their down payment assistance. KHC currently offers $10,000 for down payment assistance and sometimes throughout the year they will offer low mortgage rates on their mortgage revenue bond program.

The down payment assistance usually never runs out because you have to pay it back in the form of a second mortgage. It helps a lot of home buyers that want to buy in urban areas that cannot utilizer the USDA program in rural areas. Most of the time the first mortgage is a FHA loan tied with the 2nd mortgage fore down payment assistance. All KHC programs require a 620 score and rates are locked for 45 days.

5. What if I have had a bankruptcy or foreclosure in the past?

FHA and VA are the easiest on previous bankruptcies. FHA and VA both require 2 years removed from the discharge date on a Chapter 7. If you are in the middle of a Chapter 13, FHA will allow for financing with a 12 month clean history payment to the Chapter 13 courts, and with trustee permission.

VA requires 2 years removed from a foreclosure (sheriff sale date of home) and FHA requires 3 years.

USDA requires 3 years removed from both a foreclosure and bankruptcy, but on the foreclosure they do not go off the sale date. This may save you a little time if you had a previous foreclosure.

Fannie Mae (Conventional Loan)

Fannie Mae is by far the strictest. They require 4-7 years out of a foreclosure or bankruptcy

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people

CONFIDENTIALITY NOTICE: This message is covered by the Electronic Communications Privacy Act, Title 18, United States Code, §§ 2510-2521. This e-mail and any attached files are deemed privileged and confidential, and are intended solely for the use of the individual(s) or entity to whom this e-mail is addressed. If you are not one of the named recipient(s) or believe that you have received this message in error, please delete this e-mail and any attached files from all locations in your computer, server, network, etc., and notify the sender IMMEDIATELY at 502-327-9770. Any other use, re-creation, dissemination, forwarding, or copying of this e-mail and any attached files is strictly prohibited and may be unlawful. Receipt by anyone other than the named recipient(s) is not a waiver of any attorney-client, work product, or other applicable privilege. E-mail is an informal method of communication and is subject to possible data corruption, either accidentally or intentionally. Therefore, it is normally inappropriate to rely on legal advice contained in an e-mail without obtaining further confirmation of said advice.