Types of Kentucky Mortgage Loans to Consider After Bankruptcy

If you want to try to get a Kentucky mortgage after bankruptcy, you can research a number of different types of loans. Each mortgage loan has its own unique requirements for bankruptcy filers.

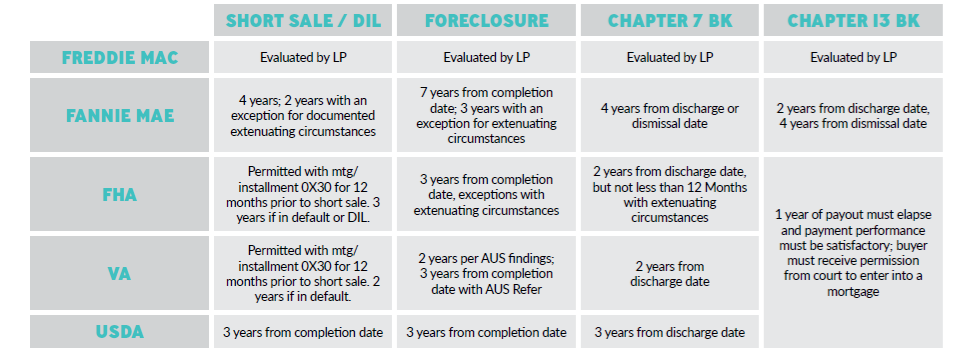

Kentucky FHA Loans

Federal Housing Administration (FHA) loans are managed by the federal government and may allow you to buy a house with a down payment that’s as little as 3.5% of the purchase price. The downfall of FHA loans, however, is that you’ll have to pay for mortgage insurance, which will result in higher monthly payments.

To get a mortgage after bankruptcy using an FHA loan, you’ll have to adhere to these waiting periods:

- Chapter 7: Two years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky USDA Loans

U.S. Department of Agriculture (USDA) loans are designed for rural borrowers who meet certain income requirements. It may be a good option if you’d like to buy a house in a rural area, have a low or modest income, and aren’t eligible for a conventional loan. If you go this route, you may not have to put any money down and you may be able to secure a low interest rate.

Keep these waiting requirements in mind if you’re interested in getting a USDA mortgage after bankruptcy:

- Chapter 7: Three years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky VA Loans

If you’re a veteran or currently serving in the military, you may be eligible for a Department of Veterans Affairs (VA) loan. A VA loan doesn’t require a down payment or charge private mortgage insurance and can give you the chance to lock in a low interest rate. If you pursue a VA loan, however, you’ll have to pay a funding fee, which will be a percentage of your home price.

Here are the waiting requirements you should be aware of if you’d like to get a VA loan after bankruptcy:

- Chapter 7: Two years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky Conventional Loans

Since conventional loans are not guaranteed or insured by government agencies, you can expect stricter requirements, such as having a good credit score, if you apply for one. If you get a conventional loan and put down less than 20% of the cost of your new home, you’ll need to pay private mortgage insurance.

The waiting requirements for taking out a conventional loan after bankruptcy are as follows:

- Chapter 7: Four years from your discharge date

- Chapter 11: Four years from your discharge date

- Chapter 13: Two years from your discharge date or four years from your dismissal date

Chapter 7 Bankruptcy

A four-year waiting period is required, measured from the discharge or dismissal date of the bankruptcy action until the application date.

Chapter 13 Bankruptcy

two years from the discharge date to the application date, or four years from the dismissal date to the application date.

The shorter waiting period based on the discharge date recognizes that borrowers have already met a portion of the waiting period within the time needed for the successful completion of a Chapter 13 plan and subsequent discharge.

A borrower who was unable to complete the Chapter 13 plan and received a dismissal will be held to a four-year waiting period.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted after a Chapter 13 dismissal, if extenuating circumstances can be documented. There are no exceptions permitted to the two-year waiting period after a Chapter 13 discharge.

Foreclosure / Short Sale

A seven-year waiting period is required. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the waiting period is the application date.

Foreclosure / Short Sale – Extenuating Circumstance A three-year waiting period is permitted if extenuating circumstances can be documented. Additional requirements apply between three and seven years, which include:

FHA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to the application date may be allowed.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to the application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to the application date is not allowed.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 2 years require manual downgrade and must be underwritten manually. Note that manual underwrites require Underwriting Management approval.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for FHA financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

Foreclosure / Short Sale

A foreclosure less than 3 years ago is not allowed.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the time frame is determined by the application date.

Kentucky VA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to application date may be disregarded.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the discharge date regardless of AUS findings.

Chapter 13

The borrower’s credit history since the bankruptcy, the circumstances behind the bankruptcy, and the discharge date all factor in to the final determination by the underwriter.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for VA financing

Foreclosure / Short Sale

Foreclosure more than 36 months prior to application date may be disregarded.

Foreclosure less than 36 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the foreclosure date regardless of AUS findings.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

USDA Guidelines for Bankruptcy and Foreclosure

Chapter 7

The Discharge date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, Chapter 7 bankruptcy seasoning is evaluated by GUS.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 3 years require a manual downgrade and must be underwritten manually.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for RD financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

• At least 12 months of payments have been made satisfactorily

• The Trustee or bankruptcy judge’s approval to enter into the mortgage transaction is documented

• Bankruptcy payments are included in the borrower’s debt ratio

Foreclosure / Short Sale

The foreclosure date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, foreclosure seasoning is evaluated by GUS.

A foreclosure does not automatically disqualify a borrower from RD financing. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

You can obtain a copy of your bankruptcy paperwork from the website below:

Bankruptcy Courts http://www.pacer.psc.uscourts.gov/

Joel Lobb (NMLS#57916)

Senior Loan Office

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.Posted by Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA Email ThisBlogThis!Share to TwitterShare to FacebookShare to PinterestLabels: 100% Financing, bad credit, bankruptcy, fico scores first time home buyer, foreclosure, Kentucky First Time Home buyer zero down payment

Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.